Las Vegas Housing Market Update - April 2023

Dropoff in Leasing Activity, But Market Conditions Look Favorable

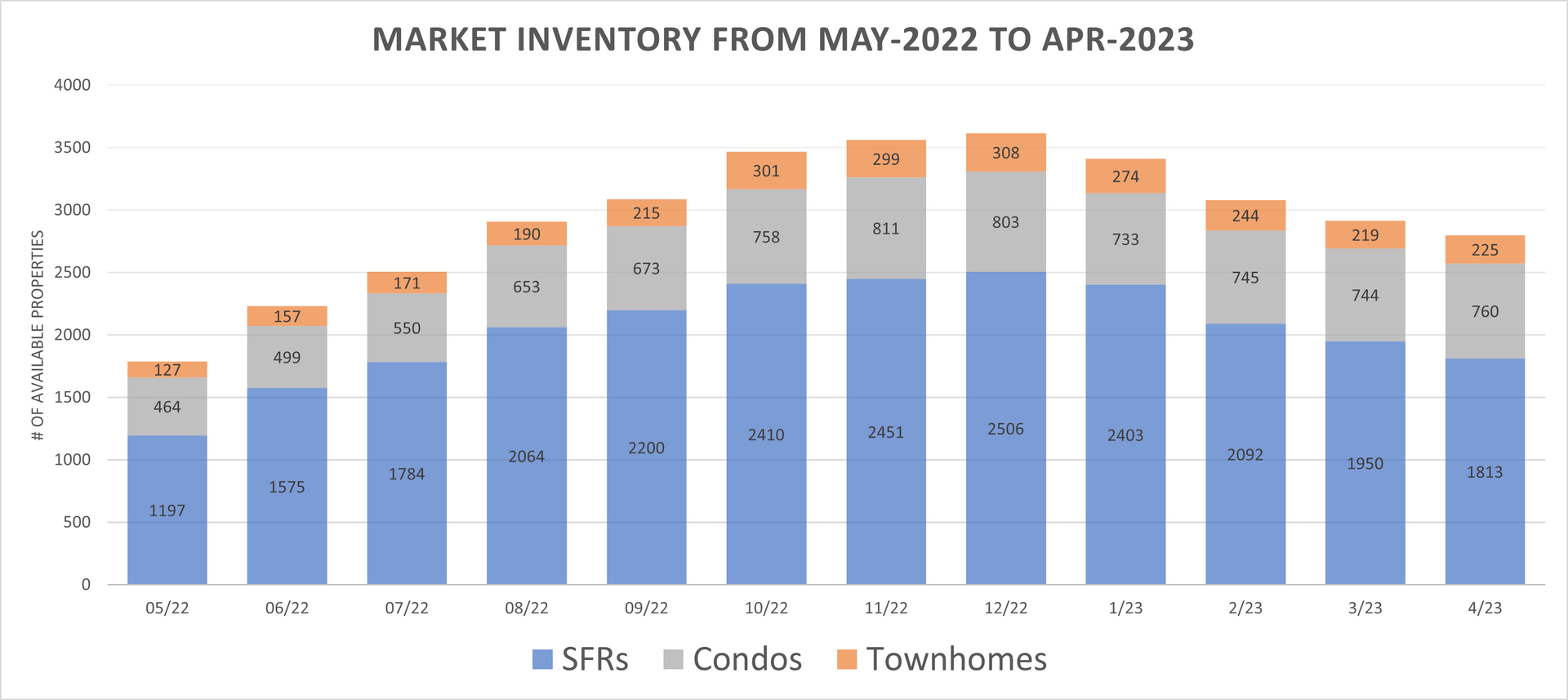

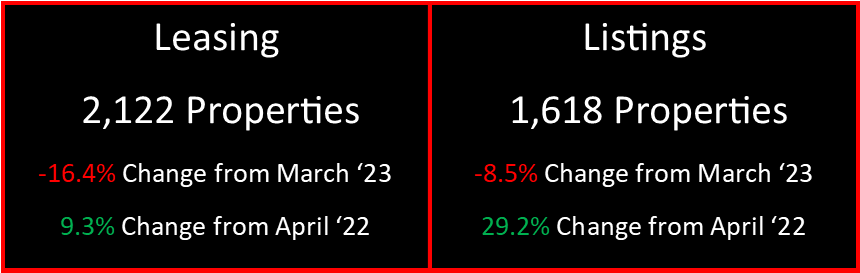

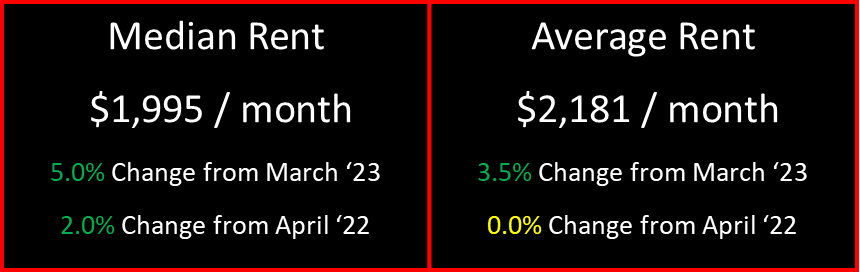

At the end of April, rental market inventory was at 2,798 rental properties, following a 4-month trend of decreasing inventory prior to the busy season. In April of 2023, 2,122 rental properties were leased across the Las Vegas Valley. This is a 16.4% decrease from March of 2023 (2,537 properties) and a 9.3% increase from April of 2022 (1,942 properties). The number of rental properties listed in April of 2023 was 1,618. This is a 8.5% decrease from March of 2023 (1,769 properties) and a 29.2% increase from April of 2022 (1,261 properties). The median price of rental properties across the valley in April of 2023 was $1,995/mo. This is the first time that median rent has increased since July of 2022, and is a 5.0% increase from March of 2023 ($1,900) and a 2.0% increase from April 2022 ($1,955). The average price of rental properties in April of 2023 was $2,181/mo. This is nearly the same average rent from April of 2022 ($2,182) and a 3.5% increase from March of 2023 ($2,107).

Here are the key takeaways for any real estate investor in the current market:

A) With increases in both median and average rent, there is potential for rental income growth for landlords and property investors. Although the pandemic disrupted the typical rental market cycle, the summer has historically been the most profitable time for property turnover. This is the period when demand is at its highest, thus tenants are less likely to shop around, and this allows for more aggressively priced rentals to be rented out. Although the changes month-over-month were nominal, this could be an indicator of a larger increase in the coming months.

B) Rental inventory is decreasing from the historic highs that were seen at the end of last year, which at first glance, may seem like positive news. However, with the additional context of over a 15% decrease in leasing activity and 8.5% decrease in new listings, a better picture is painted. April was a slow month for the market, and even with decreasing inventory, properties are, on average, still sitting on the market for over a month before being rented out. Moving into the busy season, investors and landlords should hope to see inventory numbers continue to decrease so that individual listings receive more traffic and are rented out quickly.

No matter the market conditions, every property is unique and needs a proper market analysis to determine what the current fair market rent would be. If you have questions about where your property fits into the current rental market, please reach out to us.